The US Internal Revenue Service (IRS) has introduced new rules requiring DeFi (Decentralized Finance) platforms to report user transactions, sparking concerns over privacy, feasibility, and the impact on the crypto industry. In this article, we will delve into the details of the framework, reporting requirements, effective date, and industry reaction to these new regulations.

Framework Details

The US Treasury Department released the DeFi broker tax reporting framework, mandating platforms offering trading services to report user transactions to the IRS. This move is seen as an attempt to increase transparency and accountability in the crypto space, but critics argue that it exceeds the IRS’s authority and imposes undue burdens on DeFi platforms.

Reporting Requirements

Similar to traditional market brokers, DeFi platforms must collect user transaction information and submit Form 1099 for non-wage income reporting. This means that platforms may need to include sensitive details such as names, addresses, and other identifying information in their reporting, raising concerns over privacy and data protection.

Effective Date and Impact

The new reporting requirements will take effect on January 1, 2027, and are expected to affect approximately 875 DeFi brokers. The impact of these regulations will be significant, with many platforms struggling to adapt to the new requirements and potential penalties for non-compliance.

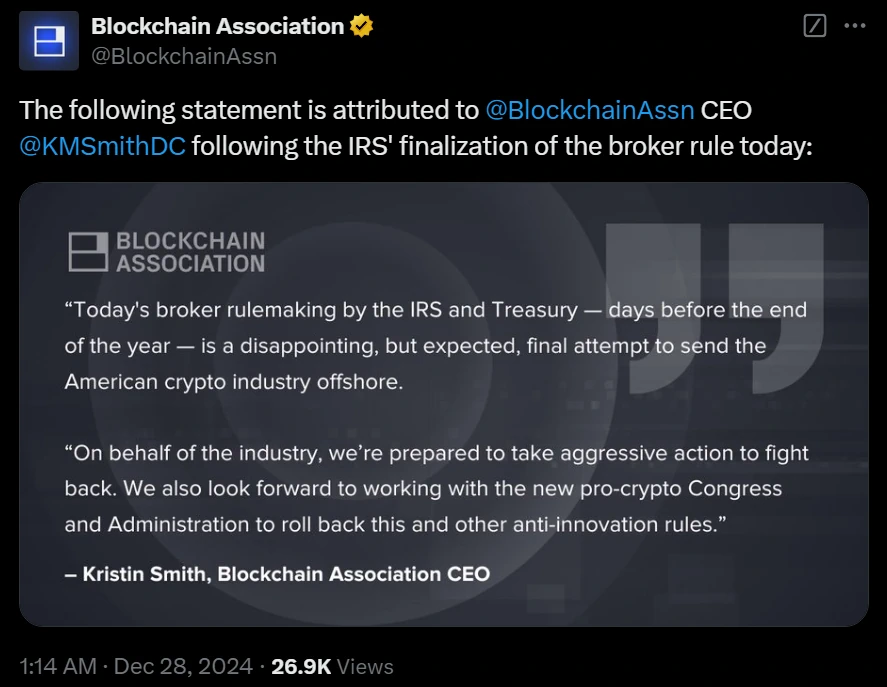

Industry and Community Reaction

The crypto community and some lawyers have criticized the IRS’s actions, arguing that they exceed the agency’s authority and impose undue burdens on DeFi platforms. There are threats of lawsuits and calls for the new administration or a crypto-friendly Congress to overturn these measures.

Concerns Over Feasibility and Cost

Industry responses, such as that from G. Blockchain Solutions, highlight the potential prohibitive difficulty and cost for many enterprises to comply with the new regulations. Critics argue that the Treasury and IRS have not adequately substantiated the benefits of the proposed rule and have refused to adopt less-burdensome alternatives.

Speculative and Unsubstantiated Benefits

Critics argue that the Treasury and IRS have not provided sufficient evidence to support the benefits of the proposed rule. The lack of clear benefits and the potential for significant costs and burdens on DeFi platforms has raised concerns among industry stakeholders.

Refusal to Adopt Less-Burdensome Alternatives

The Treasury and IRS have been criticized for not considering alternatives that might lessen the burden on smaller businesses. This has led to concerns that the new regulations will disproportionately affect smaller DeFi platforms and stifle innovation in the crypto space.

Previous Statements on Crypto Tax Crimes

In conclusion, the IRS’s new rules for DeFi platforms have sparked significant controversy and concern within the crypto industry. While the regulations aim to increase transparency and accountability, critics argue that they impose undue burdens and exceed the IRS’s authority. As the effective date of January 1, 2027, approaches, DeFi platforms must navigate the complexities of these new regulations and prepare for potential challenges ahead.